Are older households being left behind in the housing crisis?

Policy and Public Affairs Manager at the Home Builders Federation, Laura Markus, reflects on the increasing pressures of homeownership costs on older adults and stresses the urgent need for purpose-built retirement housing to support the ageing population and alleviate housing market challenges.

The increasing cost of home ownership is a widely discussed issue. While those in younger age brackets are undoubtedly shouldering the brunt of this issue, the impact on older households is often brushed aside.

With life expectancies continuing to rise, the number of older households has surged. Those aged 50 and above now make up nearly a third of the population. It’s now crucial to ensure that housing stock is not only available but also suitable for an ageing demographic.

The decline in homeownership in older adults

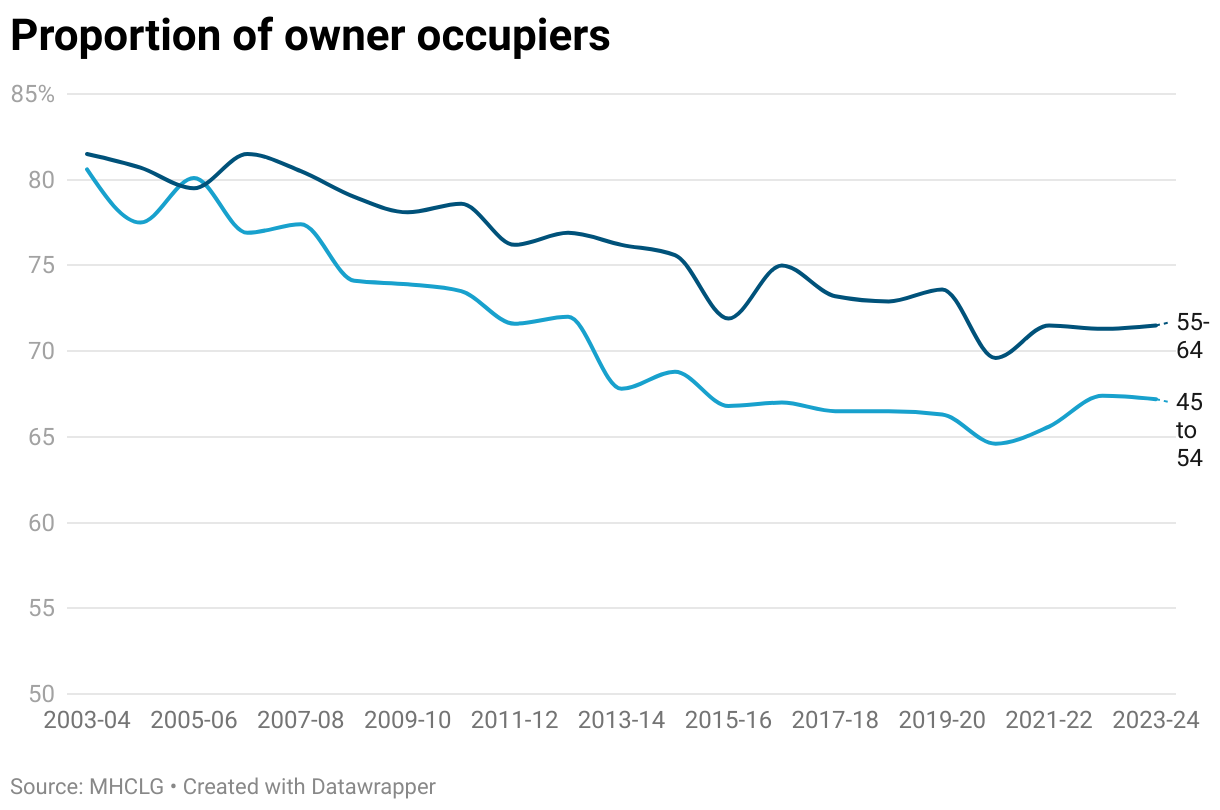

Home ownership has been declining across all age groups since the Global Financial Crisis, with tenure dropping significantly across all ages except those 65 and older.

The 45-64 age group has experienced some of the sharpest drops in home ownership, with the proportion of homeowners in the 45-54 bracket falling from 80.6% in 2003-4 to just 67.2% in 2023-4. Similarly, the homeownership rate for 55-64-year-olds dropped from 81.5% to 71.5% in the same period.

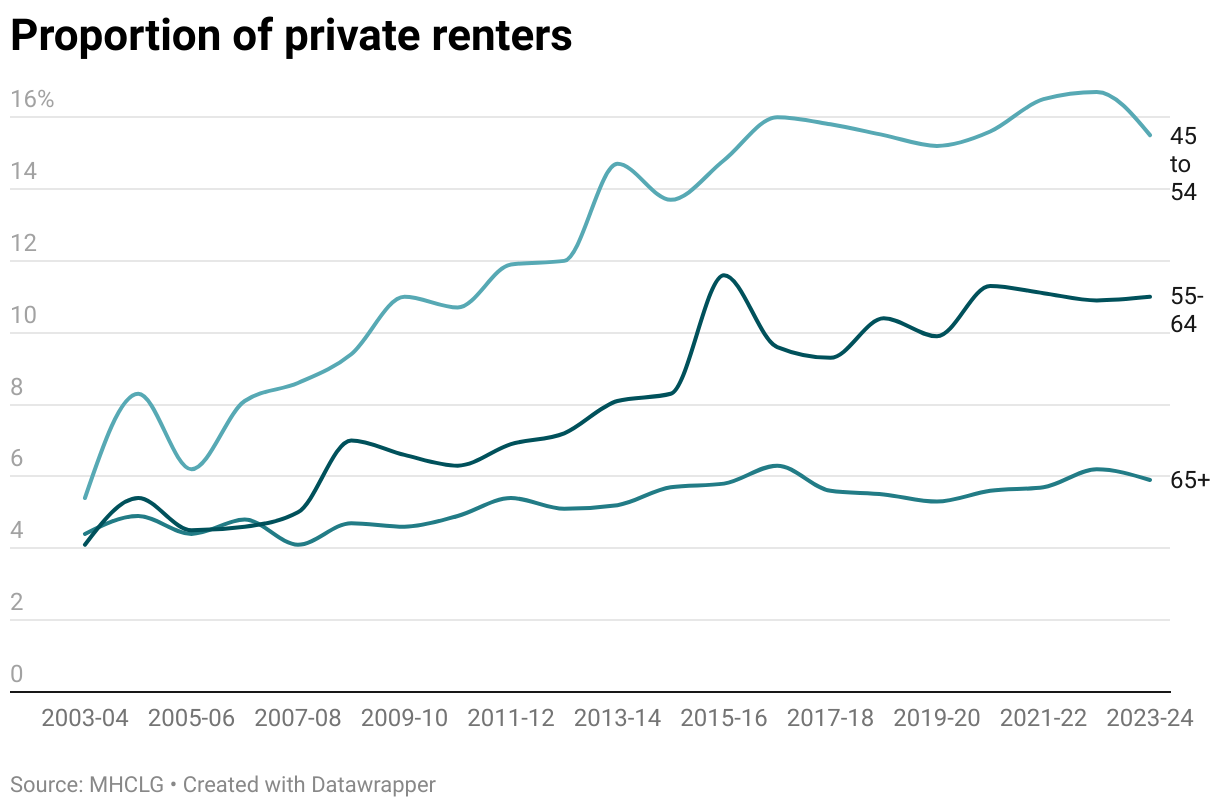

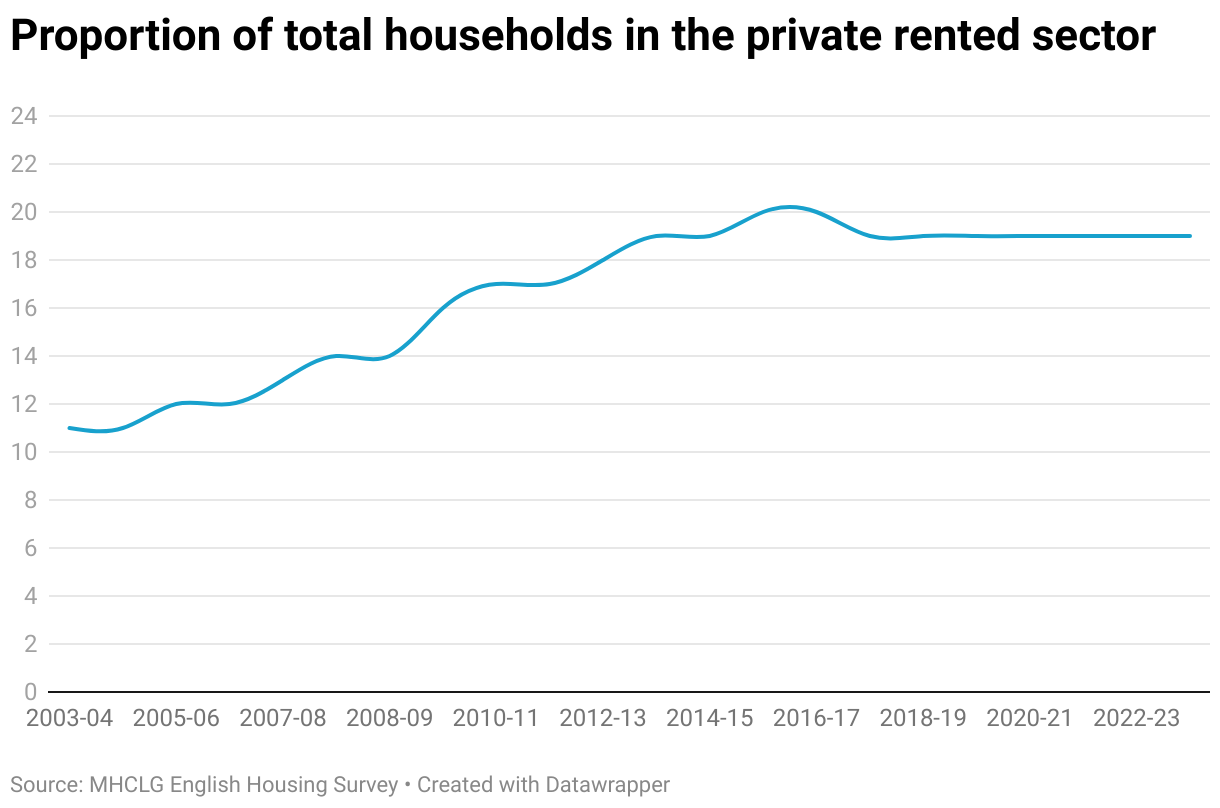

Meanwhile, the private rental market is seeing an alarming shift. The proportion of households in the 45+ age group renting privately has nearly tripled over the last 20 years. For households aged 45-54 and 55-64, this increase has been particularly stark, with those aged 65+ also facing a rise of more than a third. This is a much more significant rise than to the private rented market as a whole. Here the proportion of all households has increased from 11% to 19% over the same period.

In comparison, the proportion of all households in the private rental market has increased from 11% to 19% over the same period.

The economic pressures of private renting

The impact of this shift in patterns of housing tenure is severe and will throw up many other systematic challenges in the decades to come. Renting privately has typically been an option mostly for younger households and those without children. For older households, this could translate into financial strain in retirement.

Renting privately is often less secure and more expensive than homeownership, which leaves many older adults vulnerable to rising rents. Historically, older households could rely on the security of being mortgage-free in retirement, adjusting to lower incomes from pensions.

However, with an average income of £28,000 for those aged 50+, many older adults are struggling to meet the increasing costs of private renting, which is often outpacing their pension income of £424 per week.

The result is that older households may be forced to move away from their families and the communities they have lived in for years once they enter retirement, to areas with cheaper rent, increasing the risk of isolation and loneliness.

The social care burden

The decline in homeownership among older adults also has significant implications for the funding of social care. Traditionally, individuals who required long-term care could sell their homes to help cover the cost.

However, as the number of older homeowners decreases, a larger portion of the burden for funding social care will fall on government resources - already stretched thin by growing demand. In some areas, local councils are spending over 70% of their budgets on social care, and the shift away from homeownership could further strain these services, which are already underfunded.

The need for retirement housing

To address these challenges, there is an urgent need for more housing designed specifically for older adults, including retirement housing.

Many older adults currently live in large family homes that no longer suit their needs. The lack of appealing downsizing options has left them trapped in homes that are too big, costly, and difficult to maintain. Purpose-built retirement housing can help alleviate this issue by providing accessible, low-maintenance homes with support services, making it easier for older adults to downsize.

By encouraging older homeowners to move into retirement communities, larger homes are freed up for younger families, helping to alleviate the pressure on the housing market.

Additionally, these retirement communities can reduce the demand for social care services by promoting independent living.

Many developments offer amenities such as fitness facilities, mental health support, and social activities, which help combat loneliness and promote healthier, active lifestyles. By providing a safe and supportive environment, these communities help older adults maintain their independence for longer, while also ensuring that housing stock is used more efficiently to meet broader societal needs.

The economic impact of retirement housing

The economic benefits of retirement housing cannot be overstated. Research from the Homes for Later Living (HBF) Retirement Housing Group indicates that every retirement property sold generates at least two additional house moves further down the housing chain.

If 30,000 retirement properties were built annually, this would facilitate over 60,000 additional moves each year, easing the pressure on the housing market and contributing to its overall liquidity.

Moreover, the long-term savings to health and social care spending resulting from well-designed retirement housing could amount to £2.1 billion annually.

Addressing the housing needs of older generations

The growing number of older households and their shifting housing needs presents an urgent challenge for policymakers and local authorities.

While the general ambition to build more homes is important for all age groups, the specific needs of older adults must not be overlooked. Purpose-built retirement housing is a critical component of the solution, as it supports both the ageing population and the broader housing market.

To ensure that older adults have access to the housing they need, the government should prioritise the development of retirement housing and set a clear target of building 30,000 retirement properties each year. This would not only address the housing needs of older generations but also free up larger family homes for younger buyers, contributing to a more balanced and sustainable housing market.

Conclusion

The increasing cost of homeownership is not just an issue for younger generations. As the population ages, older adults are increasingly vulnerable to the pressures of rising rents and limited housing options.

To address these challenges, we must prioritise the development of retirement housing that meets the needs of older adults and ensures their independence in later life.

By doing so, we can reduce the financial strain on individuals and the government, while also helping to alleviate the broader housing crisis. The time to act is now to create a housing market that works for people of all ages.